The world of premium travel credit cards is larger than ever. Chase has been competing in the space with its Sapphire Reserve card, while Capital One has also put out some solid offerings such as the Venture card.

There’s one card name, however, that’s been nearly synonymous with travel since its inception: the Amex Platinum. But while this card has a storied history, how does it stand up compared to today’s premium travel credit cards? (more…)

If you’re only going to get one travel credit card, then the Chase Sapphire Preferred is an excellent choice.

It’s one of our favorite travel credit cards here at Extra Pack of Peanuts, and it was my go-to card for years (until Chase introduced the Sapphire Reserve).

Below, I’ll break down what makes the Chase Sapphire Preferred such an excellent card, but here are a few fast facts:

Earn 60,000 Chase Ultimate Rewards points after spending $4,000 in 3 months.

It’s not often that I am blown away by a credit card offer — but that changes with the Chase Sapphire Reserve.

Ever since Chase launched the Sapphire Reserve back in 2016, it’s been one of the best travel credit cards on the market.

I’ll break down exactly why below, but first, here are the important details:

Earn 50,000 Chase Ultimate Rewards points after spending $4,000 in 3 months.

$300 annual travel credit for spending on airfare, hotels, and other qualifying travel purchases.

3x on travel and dining and 1x on all other purchases.

Complimentary Priority Pass membership and a $100 credit for Global Entry or TSA PreCheck.

Sound too good to be true? Keep reading to find out all the ways this card can benefit you.

Why the Chase Sapphire Reserve Is the Best Credit Card for Travelers

The Chase Sapphire Reserve is one of our favorite travel credit cards.

So what exactly makes this card so great? Here are 7 things we love about the Chase Sapphire Reserve:

1. 50K Sign-Up Bonus with a Reasonable Minimum Spend

You’ll receive 50,000 Chase Ultimate Rewards points after spending $4,000 in the first 3 months.

Not only is 50k points a huge amount, but the minimum spend requirement of $4k in 3 months is pretty doable for most people.

2. Chase Ultimate Rewards Points

It gets better. Not only are you getting 50k points, but you’re earning the BEST travel points out there.

Chase points are my favorite because they can be used as cash through the Chase shopping portal, or they can be transferred to awesome partners like United, Southwest, and Hyatt (to name just a few).

At a minimum, these are worth $750 if you use them through the Chase portal. And if you transfer them, they can be worth $1500+.

Long story short: Chase points rule, and 50k is a lot of points.

3. $300 Annual Travel Credit

Each year, you’ll automatically get $300 in travel expenses reimbursed.

All you have to do is use your Chase Sapphire Reserve to purchase things that are coded as travel (flights, train tickets, etc.). This reimbursement is completely automatic and will show up as a statement credit.

4. Earn 3X Points on Travel and Dining

The Chase Sapphire Preferred used to be my go-to credit card because Chase points are highly valuable AND because it gives you 2x on travel and dining.

Now, the Chase Sapphire Reserve has upped the ante and gives you 3x on travel and dining.

This is awesome, especially for people who spend a decent amount on traveling and eating out.

5. Free TSA PreCheck or Global Entry

If all of that wasn’t enough, this card will reimburse you up to $100 when you sign up for TSA PreCheck or Global Entry.

TSA PreCheck will help you speed through domestic airport security, while Global Entry can save you lots of time when passing through border control both in the U.S. and abroad.

If you aren’t already a Global Entry member, we recommend getting that, as it includes TSA PreCheck.

6. Free Access to Priority Pass Lounges

All Chase Sapphire Reserve cardholders get free access to Priority Pass lounges. Priority Pass is a global network of airport lounges that offer perks such as free food, free alcohol, and free WiFi that actually works.

The lounges aren’t as luxurious as a nice hotel or restaurant, but they’re certainly nicer than the seats next to the gate.

7. No Foreign Transaction Fees

This is a standard feature with many credit cards, so Chase Sapphire Reserve isn’t special for offering it. Still, it’s a good benefit to have.

What Credit Score Do I Need for Chase Sapphire Reserve?

To qualify for the Chase Sapphire Reserve, you’ll need a Good/Excellent credit score. This generally means a score of at least 700, and ideally higher than 800. Given that the minimum credit limit for this card is $10,000, Chase wants to make you’re a responsible and experienced credit user.

Therefore, if you have average credit or just a limited credit history, we don’t recommend applying for this card. If your credit score is closer to 700, however, then it’s worth applying.

If you get rejected, you can always apply for the Chase Sapphire Preferred instead, which tends to be easier to qualify for.

Is the Chase Sapphire Reserve Worth It?

The answer depends on two factors:

How much you spend

How much you travel

Let’s take a closer look at each of these:

1. Can You Responsibly Spend $4,000 in 3 Months?

To start, if you wouldn’t ordinarily spend $4,000 in 3 months, then you shouldn’t get this card. You should never over-spend just to meet the minimum spend on a card; the math doesn’t make sense.

If $4,000 is too high, then we recommend looking into a card with a lower minimum spend, such as the Capital One Venture Rewards ($3,000 minimum) or Capital One VentureOne ($1,000 minimum).

2. Do You Travel Enough to Benefit from the Chase Sapphire Reserve Perks?

The Chase Sapphire Reserve is best for someone who travels frequently. At a minimum, you need to spend at least $300 per year on travel for this card to be worth it. Otherwise, it’s hard to justify the card’s $550 fee.

Furthermore, you need to regularly fly, stay in hotels, or do other travel-related activities to maximize the value of the Chase Ultimate Rewards points. If you tend to spend more on things like groceries and gas, then this isn’t the best credit card for you.

Our general rule is that if you travel more than 3x per year, get the Chase Sapphire Reserve. If you travel less than that, get the Chase Sapphire Preferred, which has a much lower annual fee.

Chase Sapphire Reserve vs. Preferred: 5 Key Differences

Before we conclude, there’s one more thing to address. Many people are curious about the differences between the Chase Sapphire Reserve and Preferred. The two cards share a lot of features and benefits, but there are also some key differences.

1. Chase Sapphire Preferred Has a Lower Annual Fee

The annual fee for the Chase Sapphire Preferred is $95, which is significantly less than the $550 annual fee for the Chase Sapphire Reserve. However, the $300 in annual travel credit that the Chase Sapphire Reserve offers effectively brings the fee down to just $250 if you travel regularly.

2. Chase Sapphire Preferred Has a Higher Sign-Up Bonus

Currently, you’ll earn 60,000 Chase Ultimate Rewards points when you spend $4,000 within the first 3 months of opening the Chase Sapphire Preferred. That’s 10,000 more points for the same minimum spend as the Chase Sapphire Reserve.

This difference is compelling, though you have to weigh it against the fact that the Chase Sapphire Reserve offers additional reimbursements worth up to $400 (see the next section).

3. Chase Sapphire Preferred Doesn’t Reimburse You for Travel Spending

While it’s tempting to think that the Chase Sapphire Preferred is the obvious choice given its lower annual fee and higher sign-up bonus, you also need to consider the value of the reimbursements that Chase Sapphire Reserve offers.

As we mentioned above, the Chase Sapphire Reserve will reimburse you up to $300 per calendar year for travel expenses such as airfare and hotel stays. They’ll also reimburse you up to $100 every four years for the Global Entry or TSA PreCheck application fee.

Given this, the Chase Sapphire Reserve has an effective annual fee of $250 per year (and only $150 for the first year if you apply for Global Entry). That’s still more than the Chase Sapphire Preferred, but the difference is less extreme than at first glance.

4. Chase Sapphire Preferred Earns Fewer Points for Travel and Dining

When you make travel or dining purchases with the Chase Sapphire Reserve, you’ll earn 3 Chase Ultimate Rewards points for every dollar you spend.

With the Chase Sapphire Preferred, however, you’ll only earn 2 points for every dollar you spend on travel and dining.

This isn’t a massive difference, and it really only matters if you spend a lot each month. Still, it’s worth noting.

5. Chase Sapphire Preferred Doesn’t Include Airport Lounge Access

The final important difference between the two cards is that the Chase Sapphire Preferred doesn’t include the airport lounge access that the Chase Sapphire Reserve gets you.

While this is a notable difference, it may not matter to you if you don’t spend a lot of time in airports. And while the lounges are nice, they’re far from luxurious.

Bottom Line

As soon as it was released, the Chase Sapphire Reserve became one of the best travel credit cards on the market:

The 50k sign up bonus is great, given that Chase points are the most valuable points out there.

The minimum spend is reasonable.

The $300 annual travel credit helps offset the annual fee.

Plus, you get 3x on travel and dining and a few other nice perks such as airport lounge access.

If you travel more than 3x per year and have a Good – Excellent credit score, I highly recommend you check this card out. Learn more about this card here.

Wow, it’s not often that I am blown away by a credit card offer – but that changes with the Chase Sapphire Reserve 100k offer.

Chase has just launched the Chase Sapphire Reserve, and it is, without a doubt, now the best travel credit card out there – head and shoulders above the rest.

I’ll break down exactly why below, but first, here’s the important details:

You’ll earn 100,000 Chase Ultimate rewards points after spending $4,000 in 3 months.

You also get a $300 annual travel credit, which means you’ll get reimbursed $300 every calendar year when you use the Chase Sapphire Reserve on airfare and hotels.

You’ll get 3x on travel and dining and 1x on all other purchases.

Plus, you’ll also get complimentary Priority Pass membershipand $100 credit for Global Entry or TSA PreCheck.

There is an annual fee of $550 a year, which seems steep at first, but…since you’re getting $300 a year in annual travel credit, it’s really a $150 annual fee – and you’re actually making $150 the first year, which I’ll explain below.

Why the Chase Sapphire Reserve is the Best Travel Credit Card

100k Sign Up Bonus with Reasonable Minimum Spend

You’ll receive 100,000 Chase Ultimate Rewards points after spending $4,000 in the first 3 months.

Not only is 100k points a huge amount – the biggest we’ve ever seen for a Chase card – but the minimum spend requirement of $4k in 3 months is pretty doable for most people.

Many of the higher-end credit cards – especially those with 100k point sign up bonuses – require a much higher minimum spend.

Chase Ultimate Rewards Points

It gets better. Not only are you getting 100k points, but you’re earning the BEST travel points out there.

Chase points are my favorite because they can be used as cash through the Chase shopping portal or they can be transferred to awesome partners like United, Southwest, or Hyatt.

At minimum, these are worth $1500 if you use them through the Chase portal. And if you transfer them, they can be worth $3000+.

Long story short – Chase points rule, and 100k is a lot of points.

$300 Annual Travel Credit

Each year, you’ll get $300 in annual travel credit reimbursed. This supposedly will happen automatically.

All you do is spend money on your Chase Sapphire Reserve card on things that are coded as travel (flights, train tickets, etc.) and you’ll get reimbursed.

Since this happens annually based on calendar year, the first year, you’ll actually get $600 worth of travel credit (2016 and 2017) and only pay $550 in annual fee, meaning you’re making $150!

3x Points on Travel and Dining

The Chase Sapphire Preferred has been my go-to credit card for over 4 years now because I value Chase points as the best AND because it gives you 2x on travel and dining.

Now, the Chase Sapphire Reserve up the ante and gives you 3x on travel and dining.

This is awesome, especially for people who have a decent amount of spending on traveling and eating out.

Global Entry and Priority Pass

If all of that wasn’t enough, this card gives you $100 credit when you sign up for Global Entry (if you haven’t already) and gives you Priority Pass membership.

Priority Pass lounges are decent and there are a bunch around the world, so this is a nice secondary perk, for sure.

Bottom Line

As soon as it was released, the Chase Sapphire Reserve became the best travel credit card – instantly.

The 100k sign up bonus is incredible, Chase points are the most valuable points out there, the minimum spend is reasonable, the $300 annual travel credit helps offset the annual fee (and actually makes you money the first year).

Plus, you get 3x on travel and dining and a few other nice perks.

This is a MUST HAVE travel credit card – and I’d jump on this immediately, while the bonus is at 100k.

This will be my new everyday travel card – thanks Chase for knocking it out of the park!

To see all the best travel credit cards, click the travel credit cards in the black navigation bar at the top of this page.

[UPDATE 5/12/2015: You can no longer load your REDcard with a credit card. HOWEVER, you can still load your REDcard with gift cards.

All you have to do is follow Steps 1-5, skip Step 6, and then follow steps 7-8.]

The Target REDcard (frequently referred to as a “Redbird” card due to it’s similarity to Walmart’s Bluebird card) is far and a way the best tool for anyone who wants to:

Meet a minimum spend requirement on a credit card.

Pay bills that you can’t usually pay with a credit card (mortgages, student loans, rent, taxes, etc.).

Or simply earn extra frequent flyer miles and points on your credit card.

Why?

Because it’s easy, and most importantly, totally free!

Here’s exactly how to do it:

Step 1: Find a Target that sells REDcards

The first step is actually the hardest, and that’s because at the moment only certain Target stores sell the Prepaid REDcard.

Target is slowly rolling it out to more and more stores, but it’s still in its infancy.

To check which stores currently sell Target Prepaid REDcards, click here.

If a Target near you sells Prepaid REDcards, great! Skip to Step 2.

If you don’t see a store near you listed, I’d call ones in your area and ask if they have them.

Make sure you are asking for the Target Prepaid REDcard. Stress the PREPAID part!

If a Target Near You Doesn’t Have a Prepaid REDcard:

If not, you’ll need some help to getting one. Here’s how to do that:

1. Find someone who lives near a Target who will purchase you one.

2. When that person goes to Target, have them buy an extra one for you (or many extra for multiple people).

3. When it comes time for the person to enter the birthday or social security number, they can either enter your information or enter fake information. It doesn’t matter, because you’ll have to enter your real information when you register it later.

4A. Have them send you the temporary card in the mail OR

4B. Have them open the REDcard and tell you the card number and the security code on the back.

Step 2: Buy the temporary Target Redcard

When you buy the card at Target, it’ll be a temporary card.

There are a few options, so make sure you get the Prepaid REDcard. It looks like this:

DO NOT BUY A TARGET DEBIT CARD OR TARGET CREDIT CARD! Get the Prepaid REDcard pictured above.

At the register, you’ll go through this process:

When asked how much you want to load – Make sure to load at least $1. You can load up to $500. Personally, I loaded the max ($500) so I could get more points.

Hand your driver’s license to the cashier.

Enter your birthday, social security number and phone number on the keypad.

Step 3: Register Your Temporary Redcard

If you have an existing American Express Bluebird card or Serve account you have to close that before you can register your Redcard. You aren’t allowed to have both.

Remove the sticker from the front of your temporary REDcard.

Enter the 15 digit card number and 4 digit security code that is on your REDcard. Then enter your birthday.

After that, you’ll be prompted to enter all your information.

If you had someone else buy you a Target REDcard, make sure to enter YOUR information.

You’ll get a confirmation screen saying that your permanent card is on its way.

Step 4: Use Your Temporary REDcard OR Wait For Your Permanent Card

If you want, you can use your temporary card (which only has the money you initially loaded on at Target) wherever American Express is used.

Your temporary Redcard cannot be reloaded, used at ATM’s, or used for online functions like paying bills or sending people checks.

To do all of that, you have to wait until you get your permanent card.

For that reason, I recommend that most people just wait the 4-7 days it takes to get their permanent card in the mail to start using it. This cuts down on any confusion.

If you’ve found this post, then you’re obviously interested in using frequent flyer miles. If you want to make sure you are squeezing all the value you can out of your miles, we created Frequent Flyer Bootcamp specifically for you.

Join hundreds of others who are using their miles to take some of the most amazing trips in the world. On top of that, we offer the one and only $1,000 guarantee. It’s literally completely risk-free!

Step 7 (Optional): Load Your REDcard at Target with Gift Cards

Want to get really crazy? You can also use gift cards to load the REDcard.

Why is this important?

Because you can earn even more frequent flyer miles and points!

For example:

If you have the Chase Ink Plus card, you’ll earn 5x per $1 spent at office supply stores.

That means that if you buy a $200 Visa gift card at Staples or Office Depot, you’ll earn 1,000 Chase points. Buy the gift card that looks like this:

Then, you can take that gift card and use it to load your Redcard instead of using your credit card to load your REDcard.

But why stop at one?

If you buy $5,000 worth of Visa gift cards from Staples (the amount that you can load on your REDcard each month), you’ll earn 25,000 Chase points per month.

25,000 Chase points are enough for one roundtrip ticket anywhere in North America on United!

Each $200 Visa gift card costs $6.95 to purchase. So, you’re paying $6.95 for 1,000 Chase points.

If you extrapolate that out, you’re paying:

$173.75 for 25k Chase points – a roundtrip flight in North America

$417 for 60k Chase points – a roundtrip economy flight to Europe

$556 for 80k Chase points – a roundtrip economy flight to Australia, NZ, or SE Asia

Step 8: Use Your Online REDcard Account to Pay Any Bill

Now that you have funds in your REDcard account, you can easily pay any bill you’d like from this account – including things like your mortgage, rent, student loans, or any other big expense that doesn’t normally accept credit cards.

That’s because you’ll be sending a check from your REDcard account, and almost everyone accepts checks!

If you’re struggling to visualize this, just think of your REDcard account as a bank account. It operates in the same way as a regular online checking account – it just happens to be tied to Target.

Here’s how to do it:

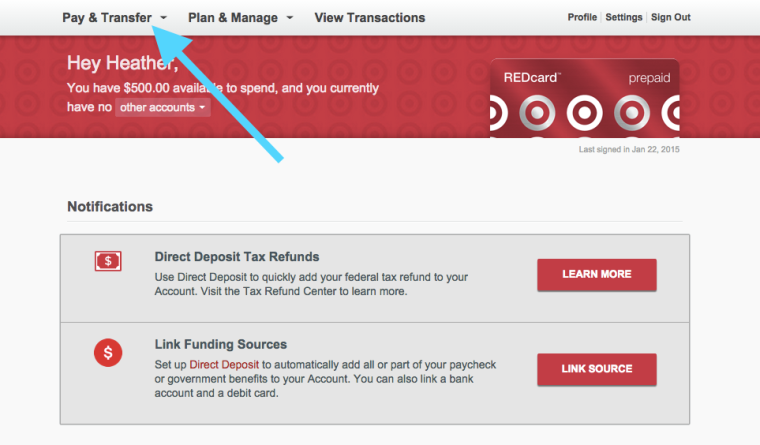

Login to your REDcard account

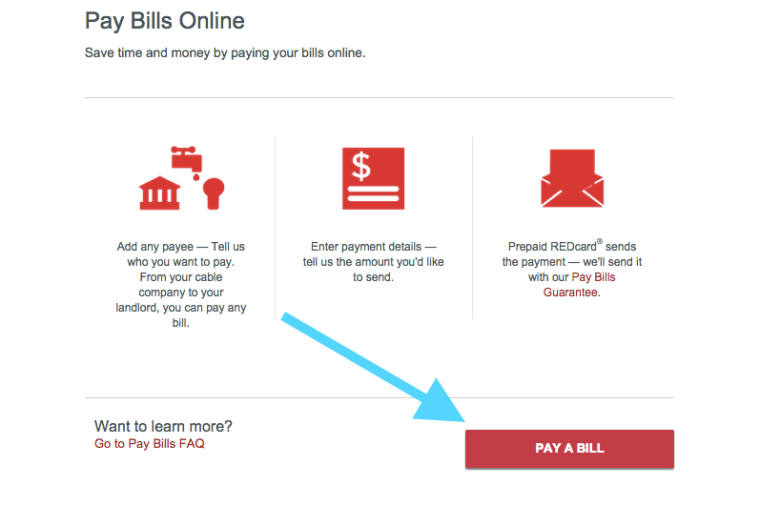

Go to Pay & Transfer and hit the Pay Bills button on the dropdown.

Hit Pay a Bill on the next screen.

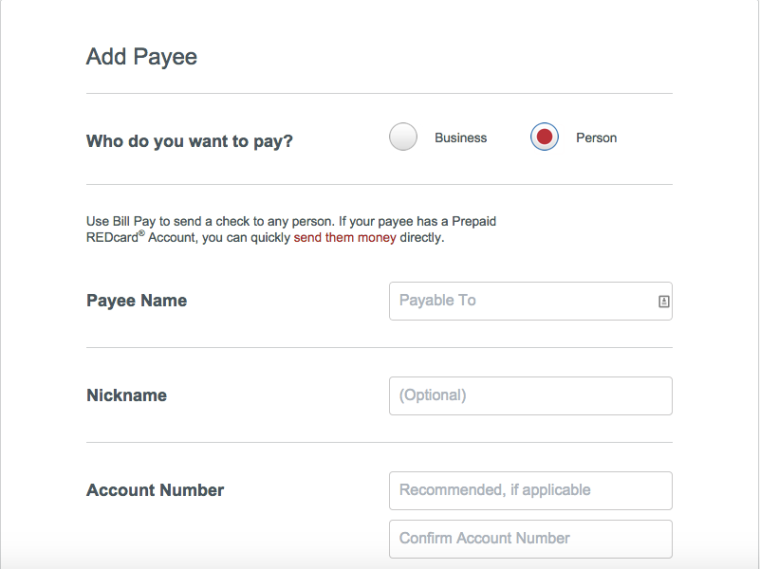

Pick whether you are paying a business or a person (if it’s a mortgage or student loan, they may have your company preloaded in the business part).

Enter the information. If it’s a person, you won’t have an account number. Hit “Save and Pay”

On the next screen, enter how much you want to pay, then you’ll hit “review”.

On the last screen, you’ll have to enter the PIN you set when you registered the card.

After that, hit “submit” and a check will be sent to whoever you are paying!

Step 9: Repeat Each Month and Rake in Points

Every calendar month, you’ll be able to add $5,000 on your Redcard.

As long as you have a Target near you, this is by far the easiest way to rack up miles and points and it doesn’t cost a cent.

If you did this for a year, you’d have 60k extra points, which is enough for a free roundtrip ticket to Europe!

2. Do you know when all Targets will start selling REDcards?

No idea.

3. Do you know when or if Targets will stop allowing us to load REDcards with credit cards and gift cards?

Nope, but I imagine they won’t let it go on forever. I’d take advantage of it as much as you can while it’s available. Personally, I’m loading the $5,000 a month max each month.

4. Can someone else buy me a Prepaid REDcard?

Yes. If you know someone who lives near a Target, they can buy you one. Then, have them either send you the temporary card in the mail or give you the card number and security code. After that, you can register it online and get a permanent card sent to your home address.

4. Is buying Target REDcards for other people illegal?

No.

5. If I’m going to buy more than one for other people, what should I say?

I simply told the cashier that I lived in Philadelphia and had driven all the way down to Maryland to get them because we didn’t have them up there yet.

I then said that my friends and family had heard about the REDcard and wanted them as well and that I was buying some for them too.

She totally understood and said she realized that only a few places had the REDcards and that it was nice of me to do that for others.

6. If someone else buys me a REDcard, do I need them to actually send me the temporary card?

No. They could open it up, give you the card number and security code, and you could “register” for your permanent card without ever actually having the temporary one in your possession.

7. How much can I load at a time?

$2,500 per day and $5,000 per month. You can only load $1,000 per swipe of your card, so if you are loading $2,500, you’ll have to ask the cashier to do it three separate times ($1k, $1k, $500).

Final Word(s)

The Target REDcard is an absolutely amazing way to meet minimum spends, get points for paying bills that you can usually pay with a credit card, or just rack up points very easily.

I highly recommend you start doing it as soon as possible, as there is no telling how long it will last.

And if it sounds a little confusing, trust me, it’s not. As soon as you do it once, you’ll realize how easy it is.

I get it, frequent flyer miles can be complicated and confusing. 2 years ago, I created Frequent Flyer Bootcamp to personally walk you through each and every step. Now, hundreds of people are traveling the world for (almost) free.

You’ll learn everything you need to know in less than one month, and we even have the one and only $1,000 guarantee.

If you thought this post was helpful in explaining a difficult subject, you’ll be blown away by our concise, easy to understand library of video lessons.