One of the most important things to know before canceling a credit card is whether or not you’ll lose your points if you cancel.

There is a lot of confusion around whether your points are safe or not, and one of the worst things you can do is cancel a card, only to find out later that you’ve lost all your hard-earned points.

Luckily, knowing whether you’ll lose your points is pretty straightforward as long as you know what TYPE of credit card you have.

The 3 types of travel credit cards

There are 3 types of travel credit cards.

Airline Credit Cards

Hotel Credit Cards

Bank Reward Credit Cards

Let’s take a look at each.

Airline Credit Cards

Short answer: Will I lose my points if I close an airline credit card? NO

These cards are specifically tied to a certain airline. The bank issues you the card and you receive the points with the airline it is co-branded with.

An example is the Citi American Airlines AAdvantage Visa.

Citi is the bank that offers you the credit card. You apply for the card through Citi, you pay the bill to Citi, etc.

However, the rewards you earn are with American Airlines.

Citi and American Airlines are two separate entities. Imagine them as two separate circles.

The credit card lives in the Citi circle, whereas the AA miles live in the AA circle.

When you close the credit card, the Citi circle disappears but the AA circle is still there.

Therefore, when you cancel an airline credit card, you still have your miles!

Hotel Credit Cards

Short answer: Will I lose my points if I close a hotel credit card? NO

Hotel credit cards operate in the exact same manner as airline credit cards, and the result is the same.

You will NOT lose your points if you cancel a hotel credit card.

An example of a hotel credit card is the Chase Marriott card.

Chase is the bank that offers you the card and Marriott is where you earn your points. They are separate circles.

Bank Reward Credit Cards

Short answer: Will I lose my points if I close my bank reward credit card? YES

We’ve saved the bad news for last. Unfortunately, with bank reward credit cards, if you cancel the credit card, you WILL lose your points.

This is because the bank is the one who gives you the credit card AND the one you have points with.

Therefore, both the card and the points live in the same circle. When you close the card, that circle vanishes, and so do your points.

Examples of bank reward credit cards include the Chase Sapphire Preferred, Amex Personal Rewards Gold or Platinum, Barclays Arrival, and Citi Thank You cards.

A Few More Answers About Bank Reward Credit Cards

How do I know if my card is a bank reward credit card?

Look at what type of points you earn with the card. Does it earn you miles specifically with airlines (United, AA, Delta, USAirways, British Airways, etc) or hotels (Marriott, IHG, Starwood, Hyatt, Hilton, etc.)?

If no, then it is a bank reward credit card. The major bank reward credit cards are ones that earn you Chase Ultimate Rewards points, Amex Membership Rewards points, Citi Thank You points, or Barclays Arrival points.

What should I do if I want to cancel a bank reward credit card but I still have points in the account?

First, ask yourself whether you should cancel the card or not.

If you decide that yes, you want to cancel the card, you have four options (in order of most to least preferable):

1. Transfer points

If they are Chase or Amex points, you can transfer them to a partner before closing the card.

For example, you could transfer your Chase points to United. Since they have been transferred, they now live in a separate circle and are safe.

In addition, Chase allows you to combine your points between accounts, meaning you can send them to another one of your accounts or to a family member’s account (check out my video tutorial on how to easily do this).

So if you have a Chase Sapphire Preferred card and a Chase Ink Bold card, you have two Chase accounts.

If you want to close the Chase Ink Bold card, you can transfer your Ink Bold points to your Chase Sapphire Preferred account. Once you transfer the points to the CSP, they are safe and you can then close the Ink Bold card.

Note: Citi Thank You and Barclays Arrival points can not be transferred, so you’ll need to look at option #2.

2. Use the points

If you can’t or don’t want to transfer your points, you can use your points “as cash” to purchase a ticket or offset the cost of a travel expense.

If you have no trips coming up to use your points on, then you can use your points to buy gift cards OR help pay off part of your credit card bill.

3. Downgrade the card and keep your points

Sometimes, the card will have a lower version that has no annual fee. If you downgrade your card instead of canceling it, most of the time you’ll be able to keep your points.

Just be aware that sometimes when you downgrade, you might lose perks.

For example, if you downgrade from the Chase Sapphire Preferred to the Chase Sapphire, you’ll keep your Chase points, but they become “limited” Chase points instead of “premium” Chase points (read about the differences here).

4. Cancel the card and lose your points

Obviously, this should be a last resort, and only done if you have a small amount of points in that account.

For example, I have 700 “straggler” Amex points in an account. They are worth $7, but it’s not enough to transfer to any partners or even cash out for a gift card (you need 1,000 minimum).

At some point, I’ll close that card and lose those points.

Final Word(s)

Before you cancel a credit card, make sure you know whether you’ll lose your points or not.

If you have an airline or hotel credit card, you can cancel a credit card and you WILL NOT lose your points.

If you have a bank reward credit card, you will lose your points if you cancel the credit card, so make sure you use them or transfer them before canceling the card.

What do you do with your points when you are canceling a credit card? Have you ever lost points by mistakenly canceling a card? Let us know in the comments below!

[offer expired] Barclays is at it again, giving us yet another awesome travel credit card and continuing to challenge the big boys of Chase, American Express, and Citi.

This time, it’s a near perfect card for people who travel domestically.

Introducing the Barclays Frontier Airlines World Mastercard®.

The Details for the Barclays Frontier Airlines Card

Here are the details of the current offer (bolding mine):

Earn 40,000 bonus miles after spending $500 in purchases in the first 90 days

Earn up to 10,000 bonus miles on balance transfers (1 mile per $1 transferred) in the first 90 days

Earn DOUBLE miles on purchases at FlyFrontier.com and 1 mile per $1 on all other purchases

No blackout dates! Book any roundtrip award flight on Frontier starting at 20,000 miles (subject to fees/taxes from $5)

Cardmember Exclusive! Redeem roundtrip companion award tickets for 5,000 less miles (from 15,000 miles plus taxes/fees from $5)

0% Introductory APR on purchases and balance transfers for the first 12 months after account opening. After that, a variable APR, currently 15.99% or 24.99% based on your creditworthiness

$69 Annual Fee

Click here to apply —> Barclays Frontier World Mastercard®

Why I Love the Barclays Frontier Airlines Card

Reason #1: 40,000 mile sign up bonus

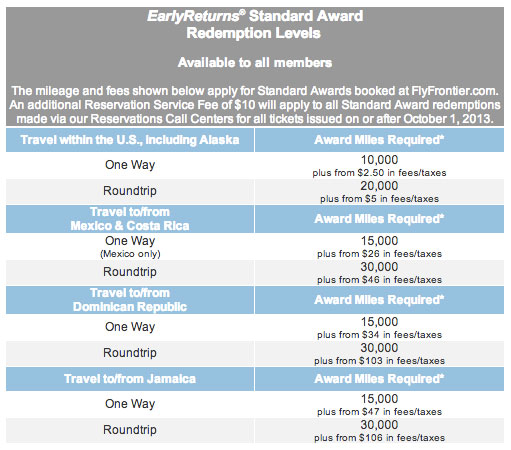

40,000 miles is a good sign up bonus nowadays, especially considering the Frontier airlines award chart.

The 40k sign up bonus can get you 2 free roundtrip tickets anywhere in the US, including Alaska!

Check it out:

Or, since they allow one way tickets, you could use it for 4 free one-way tickets.

It can also get you 1 free roundtrip ticket to either Mexico, Costa Rica, or Jamaica and you’d have miles to spare!

Most airlines charge 25k miles roundtrip for a domestic ticket, so the fact that Frontier only charges 20k is huge.

This is a great sign up bonus for domestic travelers.

Reason #2: The Low Minimum Spend

In order to get the sign up bonus, you’ll only need to spend $500 on the card in the first 90 days.

Most other cards require much larger minimum spends, such as $3,000 or $5,000 in the first 90 days.

The $500 minimum spend means that this is a card that ANYONE can meet the minimum spend on.

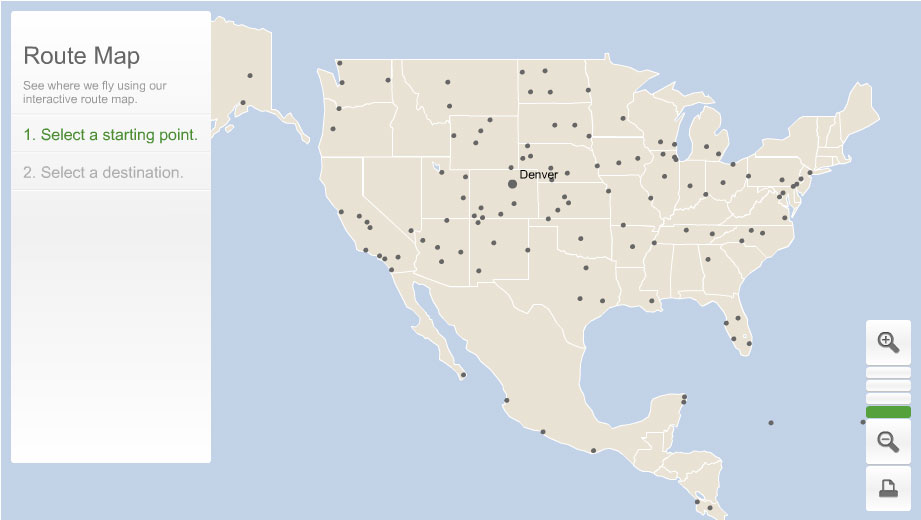

Reason #3: Frontier Airlines Flies From Lots of Smaller Airports

For people who don’t live near large hub airports, this is a MASSIVE benefit.

Here is a map with all the places that Frontier flies to:

This is especially good for people out in the west and midwest, as Frontier flies to places like Jackson Hole, tons of places in Kansas and Nebraska, and even 5 different airports in North Dakota (wow!)

It’s even really great for people who do live near major airport.

For example, I live about 45 minutes from Philadelphia International (PHL).

Frontier flies out of PHL, but also flies out of 3 other airports in the area, including Wilmington (ILG), Trenton (TTN), and Harrisburg (MDT).

Not only does this give me a ton of options, but flying out of a smaller airport is also oftentimes a better experience.

It’s usually easier to get to, not as hectic to go through security, and parking is cheaper or even free!

Reason #4: Companion Tickets are 5k Less

With the Barclays Frontier Airlines card, you’ll receive a companion ticket. Here’s how the Frontier Companion Ticket works.

If you purchase a ticket with cash on Frontier, a companion can fly using miles for 5k less than the normal price.

This means that instead of paying 20k for a domestic roundtrip ticket, you’d only pay 15k.

And it can be used on one-way tickets as well!

Since a one-way domestic ticket is only 10k, you’ll actually only pay 5k miles + $5 using the Companion Ticket.

That’s a sweet deal!

Just remember, you can only use the Companion ticket if you PURCHASE your ticket with cash.

So if you have two people traveling and find a cheap ticket on Frontier, consider purchasing it the first one and having the companion fly on miles for cheap!

Reason #5: Cheap Changes on Award Tickets

One way most airlines really gouge you is when you have to make changes to an award ticket after you’ve booked it.

Luckily, Frontier isn’t like most other airlines.

Any change you want to make to the itinerary of an award ticket that is more than 8 days before you leave is free.

Also, if you want to cancel the ticket and have your miles redeposited in to your account, it’s only $75 (most airlines charge you $150).

Click here to apply —> Barclays Frontier World Mastercard®

Downsides of the Barclays Frontier Airlines Card

Overall, I think this is phenomenal card for anyone who is traveling domestically and really is a must-have.

However, there are two downsides.

$69 Annual Fee

The $69 annual fee is NOT waived the first year. I consider it a very small price to pay.

In essence, you’re paying $69 for two roundtrip tickets, which is a great deal.

Still, it’s something to be aware of.

Frontier Charges for Checked Bags

If you do use miles, Frontier charges $25 to check the first bag, and $30 for a second checked bag.

Of course, carry-ons are free, and I always recommend traveling with just a carry-on anyway, so this isn’t a big deal to me.

But if you’re someone who does check baggage, just make sure you are aware of the fees (which are actually less than most airlines).

Final Word on the Barclays Frontier Airlines Card

All in all, I believe the Barclays Frontier Airlines card is one of the best card right now for domestic travel and I HIGHLY recommend it.

The sign up bonus of 2 free roundtrip ticket, even to Alaska, is awesome.

The minimum spend is super low.

You can fly one-way if you want.

And as an added bonus, you can also fly in to and out of some really cool, easy small airports that aren’t serviced by most other airlines.

Add it all up, and you’ve got another great travel credit card from Barclays!

Now that the sign up bonus is 40k, are you going to apply?

If so, what cool city that Frontier flies to do you have your eye on?

If you do apply for the Barclays Frontier card using my links, I’ll receive a commission. Your support allows me to continue to run this site full time and as always, is truly appreciated!

Personally, I’d be more inclined to use the free things, such as the bikeshare (and will definitely use it next time I’m there), but some of the events are pretty fascinating and can make for a fun night out, especially if you’re traveling to a city and looking for something unique.

Then, head to the Priceless City page of your choice and purchase the event or deal with a World Mastercard.

For example, to purchase the sushi rolling class, I’d head to the Priceless City New York page and then purchase it online.

For coupons to free things, such as the Citi Bikeshare program, you’ll head to the Priceless City New York page, enter your details, and then be given a coupon code to use.

It’s super simple, just make sure that for whatever you are buying to use your World Mastercard to be eligible.

Bottom Line

Since it doesn’t cost you anything extra, there is absolutely no reason not to take advantage of this great perk that Mastercard offers.

Pick a city, browse through the deals they offer (which in some cities, is A LOT), and see what you like.

Each one of those cards will make you eligible for the Priceless Cities perk.

Personally, I’d suggest the Barclays Arrival and the Barclays USAirways card, as they offer the best sign up bonuses at the moment.

If you’ve had them before and closed them, then maybe take a look at the Lufthansa Miles & More or Citi AA Mastercard, but the sign up bonuses at the moment are pretty weak.

Has anyone taken advantage of a cool Priceless Cities perk? After looking through the list, anything intriguing to you? Let me know in the comments below!

If you use one of my links to sign up for a World Mastercard, I may receive a referral. As always, I appreciate the support.

Today at EPoP its time to get personal. I feel like we’ve reached that level in our relationship; it’s been 8 months, after all. Shouldn’t we reveal stuff to each other? So today, I’m going to let you in on a little secret, something I haven’t mentioned before on the blog….

I’M A TWIN!

Yes, it’s true. There is another 29 year old out there in this world (currently Spain) who shares the same birthday, same set of parents, and same upbringing as myself. Scary, huh? Luckily for my twin, we aren’t identical. You see, she’s a girl.

(quick side note: You won’t believe the number of people (at least 500 in my life) who know that I have a twin SISTER and ask me if we are identical twins. Usually, I ask them why their school didn’t offer health class in 5th grade.

When this baffles them, I remind them that “boys” and “girls” have different body parts, thereby not allowing them to be identical. It’s amazing the questions science can answer!)

And while there is one major difference between my sister and I, we tend to share a lot of the same qualities, neurosis, and quirks (for better or worse). The Chase Ink Plus and the Chase Ink Bold are very similar in this way. [The Ink Bold Card is no longer available from Chase]

One Major Difference

Danny and Arnold…more than one major difference!

The one major difference between the Chase Ink Bold and the Chase Ink Plus is that the Ink Bold is a CHARGE card while the Ink Plus is a CREDIT card.

This is an important distinction.

Since the Ink Bold is a charge card, the balance must be paid in full each month. You can not roll over a balance from month to month. You MUST pay the full amount each month.

The Ink Plus is a credit card, which means that you can carry a balance on it from month to month. I NEVER, EVER recommend carrying a balance because the interest you are paying on that balance negates any frequent flyer benefits you are getting from the card, but the Ink Plus will allow you to do so if you need to.

The Similarities

Mary Kate and Ashley…not identical, but pretty close!

Outside of the charge card vs. credit card difference, EVERYTHING ELSE about these two cards is the same. The Ink Plus has all the awesome, amazing perks that the Ink Bold has. And if you’ve been following this blog for any length of time, you know that I LOVE the Ink Bold, so if you guessed that I LOVE the Ink Plus, you’d be spot on. It’s an awesome, awesome card!

So instead of writing another 1,300 word love letter to the Ink Plus, I’ll just point you towards the one I wrote to the Ink Bold (it’s right here, my first public love letter) and each time you read “Bold”, substitute “Plus”. Remember, they’re twins!

For those of you who don’t feel like reading my eloquently written love letter, here is a list of the awesome perks that the Ink Plus and Ink Bold share:

Signup bonus of 50k Chase Ultimate Rewards points (transferable to United and Hyatt, among others) after spending $5,000 in 3 months.

5x for every $1 spent on cable, internet, and cellphone bills

5x on every $1 spent at office supply stores (including gift cards, which means you can buy gift cards and essentially get 5x on every purchase you make!)

2x on gas, a huge bonus when the gas is at $4 a gallon!

2x on hotels and motels

1x on everything else

$95 annual fee WAIVED FOR THE FIRST YEAR

No foreign transaction fee

There is ALOT to like about this card.

Of course, the one major complaint about the Ink Bold and Ink Plus cards is the minimum spend requirement, which is $5,000 in 3 months.

Only get this card if you can definitely hit the minimum spend requirement. $5,000 in 3 months can be steep for some people, so always err on the side of caution.

If you can’t meet the $5k requirement, there are plenty of other options listed on the Best Current Deals page.

The Big Question: Can You Get Both Cards?

Twins having their cake and eating it too!

This is an emphatic YES!

Even though these cards are “twins”, they are considered different cards by Chase and therefore you are eligible to earn the signup bonus for BOTH cards.

Final Word(s)

Psssttt….I don’t really think you have to be a twin to love a twin.

In fact, the Chase Ink Plus is such an AWESOME card and I’d recommend it to EVERYONE who thinks they can meet the minimum spend requirement, single, twin, triplet, or otherwise!

The 50k bonus is great and the bonus categories allow you to rack up tons of extra Chase UR points.

Most importantly, you’re eligible to get the signup bonus for the Ink Plus even if you already have the Ink Bold since it is considered a different card by Chase.

When you’re flying free on United or staying at uber-posh Hyatts you’ll be glad you applied for this card!

The first question I usually get asked when I begin regaling (or annoying) people with my tales of traveling around the world for free is “Are you rich?”. As soon as the chuckle escapes my lips, the person immediately follows up with “Well, is your wife rich?”.

Again, I chuckle, and then begin explaining that I use frequent flyer miles to travel. Question three is usually “how many freakin’ credit cards do you have?”.

As I enter my second full-fledged year in the the frequent flyer mile game, and prepare for my summer App-o-rama, I figured now was as good a time as any to take stock of the cards I have.

I’ll reveal which cards I prefer to use to maximize my points, and then ultimately decide which ones are worth keeping based on the anniversary bonus they offer and the annual fee they charge.

Hopefully, this will help prove useful for the many of you out there who are facing many of the same decisions of closing or keeping open accounts and also deciding which cards you should add to your stable.

I’ll list the cards in chronological order of the date I got them.

Without giving away the answer, I will tell you to settle in and get comfortable, because the number is quite large.

Sooo….how many cards do I have?

1. Citi/AAdvantage Visa

See Best Current Deals page for further breakdown of this card, how to get both the Citi/AA Visa and Amex at the same time, which I highly recommend doing, and the application links for these cards

Signup bonus: 75k when I got it, 50k now

Date approved: July 29, 2011

What I use it for: Nothing after meeting the minimum spend and getting the signup bonus.

Annual fee: $85

Anniversary bonus: Nothing

Odds of keeping it open after 1 year: 25%. If I call in to cancel and they over me a great retention bonus (7,000 AA miles or more, an $85 statement credit, etc) than I’ll keep it open. If not, thanks for the signup bonus but this card is history!

2. Alaska Airlines Visa

Signup bonus: 40k when I got it, 25k now

Date approved: August 8, 2011

What I use it for: Nothing after making the first purchase and getting the signup bonus.

Annual fee: $75 (not waived the first year)

Anniversary bonus: $99 companion pass.

Odds of keeping it open after 1 year: 0%. If I made good use of the companion pass than this card might be worth keeping open. However, I didn’t use the companion pass this past year, so I’m assuming I won’t make use of it this upcoming year either. Plus, you can “churn” this card and get the signup bonus again, so if I’m going to pay the fee, I might as well get the extra 25,000 as a bonus again!

3. Chase Sapphire Preferred

Signup bonus: 50k when I got it, 40k now

Date approved: August 22, 2011

What I use it for: Almost all my everyday spending. I especially focus on using it for travel and dining, which earns me 2x. Since I live abroad, I use this card all the time because it has no foreign transaction fee.

Annual fee: $95 (waived the first year)

Anniversary bonus: 7% bonus on all points earned, including the signup bonus.

Odds of keeping it open after 1 year: 100%. This is my favorite card and my go-to for almost all of my spending. I love that it has no foreign transaction fee and also that it gives me 2x for travel and dining. I almost always transfer my Chase UR points to United miles, which I love. The 7% bonus is nice too, although I wouldn’t consider just that enough to keep the card open. I’ll keep it open because I love the everyday earning potential!

What I use it for: Occasionally, and sporadically, for groceries because it offers 2x on groceries and gas. However, I don’t even usually use it for airfare, which it offers 3x on, because I’d rather the 2x Chase points (for travel by using the Sapphire) than the 3x Amex points.

Annual fee: $175 (waived the first year)

Anniversary bonus: None.

Odds of keeping it open after 1 year: 0%. The 3x on airfare and 2x on gas and groceries could be lucrative for some people but I don’t really put much value Amex points because they don’t offer good transfer partners. I’d rather use my Sapphire for 2x on travel and my Ink Bold for 2x on gas and build up a nice point balance through Chase and then transfer those points to United. The $175 is too high a fee to justify the extra points I’d get for spending on groceries.

5. Barclays USAirways Mastercard #1

Signup bonus: 40k

Date approved: September 25, 2011

What I use it for: Nothing after the first purchase to get my signup bonus and once every 6 months to adhere to the terms and conditions.

Annual fee: $89 (waived the first year)

Anniversary bonus: 10k USAirway miles

Odds of keeping it open after 1 year: 100%. The 10k USAirways miles are worth over $89 for me so this is a no-brainer. I’ll whip it out every 6 months and use it once just to make sure I’m abiding by the terms and conditions, but other than that, it’ll collect dust on the shelf.

6. American Express Hilton HHonors

Signup bonus: 60k when I applied, 40k now

Date approved: November 9, 2011

What I use it for: Nothing after meeting the minimum spend and getting the signup bonus.

Annual fee: $0

Anniversary bonus: None.

Odds of keeping it open after 1 year: 75%. Normally, this would be 100%, as it never really makes sense to close a card with no annual fee. However, it is being reported that some people have had success getting this card and the signup bonus again after closing their original card. If that is the case, I may close this card so that I’m eligible to get the bonus again. If not, then I’ll just leave it open indefinitely.

7. Chase Marriott Rewards Premier Visa

If you apply for this card, the application page will show a 50k signup bonus. Many people have reported that Chase will honor the 70k offer if you ask them to “bump the bonus” through a secure message after applying.

Signup bonus: 70k + 1 free night in a category 1-4

Date approved: November 9, 2011

What I use it for: Nothing after making the first purchase and getting the signup bonus.

Annual fee: $85 (waived for the first year)

Anniversary bonus: 1 free night at a category 1-5 each year.

Odds of keeping it open after 1 year: 65%. This one will be a tough decision. If used right, the one free night can easily be worth up to $150, which more than makes up for the annual fee. However, I usually prefer to stay at locally run boutique hotels and hostels when I go on vacation. If I needed to “go out of my way” to use the free night, then it wouldn’t be worth it.

Odds are that I’ll keep this open, not only for the free night but also because keeping cards open helps your credit score and having this card open will give me more leverage with Chase when trying to get other Chase credit cards…Ok, basically I just talked myself in to keeping it open!

8. Chase Ink Bold Business (old version)

Signup bonus: 50k

Date approved: November 9, 2011

What I use it for: Nothing after making the minimum spend and earning the signup bonus.

Annual fee: $95 (waived for the first year)

Anniversary bonus: None.

Odds of keeping it open after 1 year: 0%. Now that I have the new Chase Ink Bold card (which is much better), there is no point at all for me to keep this card open.

9. Citi Thank You Premier

Signup bonus: 50k

Date approved: November 9, 2011

What I use it for: Nothing after making the minimum spend and earning the signup bonus.

Annual fee: $125 (waived for the first year)

Anniversary bonus: 1% on all Citi TY points earned through purchases (does not include the signup bonus)

Odds of keeping it open after 1 year: 0%. There are a few reasons I won’t be keeping this card open; the $125 is super high for a card of this (low) caliber, the anniversary bonus is of little value since I don’t put any spend on this card, and Citi TY points are not that valuable compared to Chase UR points.

Lastly, I had to fight tooth and nail with Citi not only to get this card, but also for them to credit me with the signup bonus (think 10+ emails and even snail mail letters) so needless to say, I’m not a fan of their company or their customer service.

10. Barclays USAirways Mastercard #2

This is the exact same card as #4.

Signup bonus: 40k

Date approved: April 3, 2012

What I use it for: Nothing after the first purchase to get my signup bonus and once every 6 months to adhere to the terms and conditions.

Annual fee: $89 (waived the first year)

Anniversary bonus: 10k USAirway miles

Odds of keeping it open after 1 year: 100%. The 10k USAirways miles are worth over $89 for me so this is a no-brainer. I’ll whip it out every 6 months and use it once just to make sure I’m abiding by the terms and conditions, but other than that, it’ll collect dust on the shelf.

What I use it for: Nothing after the first purchase to get my signup bonus. However, if I were to purchase United tickets, I would use this card to get the 3x on United purchases.

Annual fee: $95 (waived the first year)

Anniversary bonus: 2 free United Club lounge passes each year.

Odds of keeping it open after 1 year: 60%. I’m completely on the fence about this one. The lounge passes are nice (and $100 retail value) but I debate how much I actually value them. Sure, its nice to have lounge access for a day, but I normally wouldn’t pay $50 for that privilege.

However, the card does also offer a free checked bag ($50 value) on United flights and like the Marriott above, gives me leverage with Chase when I go to apply for other cards. Those two reasons will probably be enough to push it over to the “keep” side, but I’m glad I have a while to decide!

12. Chase Southwest Rapids Reward Business card

Signup bonus: 50k

Date approved: April 3, 2012

What I use it for: Nothing after the first purchase to get my signup bonus.

Odds of keeping it open after 1 year: 60%. I know I sound like a broken record, but I’m slightly leaning towards keeping this open just to have leverage with Chase. The 3,000 points aren’t enough to justify the annual fee (although it’s close), so what I’ll most likely do is keep this card open for the time being.

When I go to apply for other Chase cards, they may say I have too many accounts open with them, and that time, I’ll happily give up my Southwest account in order to get a new card and the signup bonus.

13. Chase Ink Bold Business (new card)

This card is no longer available. The Ink Plus is still available.

Signup bonus: 50k

Date approved: April 23, 2012

What I use it for: Cable, cellphone, and internet bill (5x points), gas (2x) and gift cards from office supply stores (5x) that help me earn a TON of Chase UR points. I also flip-flop the Ink Bold and the Sapphire Preferred for everyday spend items that don’t fall in those categories.

Annual fee: $95 (waived the first year)

Anniversary bonus: None.

Odds of keeping it open after 1 year: 100%. I absolutely LOVE this card. The fact that I can buy gift cards at office supply stores for all types of products and get 5x for them is amazing and keeps the points continually rolling in.

The only downside to this card is the high minimum spend in the beginning (although there are tons of ways to make it easier than you think), so now that I’ve hit that, I’ll keep using the awesome earning power of this card for years to come!

Recap

As do I! If it’s a good bonus, I’m there!

If you’ve been tallying the cards up mentally, you’ll see that I currently have a total of 13 cards. Many people ask me how I manage to have all those cards and not get confused, but if you break it down, you’ll see that I have:

2 that I use for everyday spending (Chase Sapphire Preferred and Chase Ink Bold)

1 that I pull out very occasionally (Amex Personal Rewards Gold)

10 that basically go unused after making the minimum spend

In reality, I’m not juggling 13 cards, but really only 2. Most of the time I’ll carry one of them and my wife will have the other. Pretty simple.

People also always ask me how I keep track of all of them and how I know when to cancel them.

I employ a simple system that even a caveman could understand; I use a really basic Excel spreadsheet (feel free to EPoP Credit Card Tracking Template) which lists when I need to cancel each card.

Additionally, if you do App-o-Ramas it is easier to keep track of your cancellation dates because a bunch of the cards fall on the same day! Yet another perk of the AoR!

Lastly, here is the breakdown of which cards I will and won’t keep after the 1st year and pay the annual fee for:

4 On the Fence- Chase Southwest, Chase United Explorer, Chase Marriott, Amex Hilton

5 Definitely Closing- Citi Thank You Premier, Chase Ink Bold (old), Amex PRG, Citi/AA Visa, Alaska Airlines Visa

As you can see, having a large amount of open accounts doesn’t have to be scary or difficult to manage. Pick a few cards that you prefer to use for everyday spending and then supplement them with cards that you’ll use for the signup bonus and then close after a year.

That way, it only takes a tiny bit of brain power and small amount of organization to keep you on top over everything.

Disclaimer: This content is not provided or commissioned by the credit card issuer. Opinions expressed here are author’s alone, not those of the credit card issuer, and have not been reviewed, approved or otherwise endorsed by the credit card issuer. This site may be compensated through the credit card issuer Affiliate Program.

Unfortunately the Chase Ink Bold card is no longer available from Chase.

The information in this post is still relevant when applied to the Chase Ink Plus card, which is almost identical to the Ink Bold.

The Chase Ink Bold is one of my absolute favorite cards, and is a no-brainer for any business owner.

Why?

Here are the top 6 reasons that the Ink Bold has stolen my heart.

But first, the details:

The Details for the Chase Ink Bold

Earn 50,000 bonus points after you spend $5,000 in the first 3 months from account opening. That’s $625 toward travel when you redeem through Chase Ultimate Rewards.

No interest charges because you pay your balance in full each month.

Earn 5X points per $1 on the first $50,000 spent annually at office supply stores, and on cellular phone, landline, internet, and cable TV services.

No foreign transaction fees.

Direct access to a live service advisor anytime.

1:1 point transfer to leading frequent travel programs with no transfer fees.

$0 Intro Annual Fee for the first year, then $95.

Click here to apply for the Chase Ink Bold

Why I Love the Chase Ink Bold

Reason #1: 50,000 point signup bonus

With a sign up bonus of 50k points, this is one of the largest available bonus out there.

You’ll get 50k after spending $5,000 in 3 months.

50k points is great in any situation, but its even better when its earning you….

Reason #2: Chase Ultimate Rewards Points

If you are not familiar with Chase Ultimate Rewards points, I suggest you get acquainted quickly because they one of the most valuable currency out there in the frequent flyer world. The Ultimate Guide to Ultimate Rewards will answer all the questions you may have about these awesome points!

These Chase UR point have tremendous value because they can be transferred to a ton of partners, both airlines (United, Southwest, Korean, BA) and hotels (Hyatt, Marriott, Priority Club, Ritz-Carlton).

All of these transfers are at a 1:1 ratio and they all transfer instantly, a huge plus if you have a penchant for waiting until the last minute or need to take advantage of a deal quickly.

My favorite transfer is to United because you’ll never pay a fuel surcharge when using United miles and they are part of Star Alliance, which not only has good award availability but also has partners that fly to anywhere in the world!

Chase points are my personal favorite and I earn them at every possible opportunity. Start earning Chase UR points now and you’ll never look back!

Reason #3: 5x on cellphone, cable, and internet bills

If you’re the .01% of Americans that don’t have either a cellphone, cable, or the internet then this won’t excite you as much as 99.9% of us who do.

I LOVE this perk of the Ink Bold because it’s so easy to do. Simply change your cellphone, cable, and internet bills over to be paid by your Ink Bold card and you’ll automatically receive 5x Chase UR points for every $1 you spend. Set it and forget it!

This is an especially huge score for people who pay for a family cellphone plan with a bunch of phones or have 1,000 cable channels and pay pretty hefty bills each month. When I last lived in the States I was paying about $200 a month between my cellphone, cable, and internet (a fairly normal amount I think).

By putting this spend on the Ink Bold, I’d pull in 1,000 UR points a month, 12,000 a year. All for doing nothing! Free and effortless points? I’ll take that any day!

Reason #4: 2x on gas

I’ve yet to run in to a person who has said “You know, I just really love paying $4 a gallon for gas.” I know, I know, hard to believe, right?

The truth is, paying that much for gas SUCKS. Unfortunately, we better get used to it.

Most other developed countries have been paying this much and more for years now, and if we are being realistic, it’s obvious that the gas prices in America are never going to go back to anything close to what they were pre-Katrina.

$4/gallon is here to stay.

So you have two options:

Nothing screams sexy like a Prius!

Get a Prius

Get the Ink Bold

While paying $4 a gallon might suck, getting 2x UR points for every $1 you spend at the pump can help ease the pain. You’ll receive 2x for the first $50,000 you spend each year on gas, so unless you’re dropping a grand a week on gas, all your gas spending will net you 2x/$1.

And if you are one of those unfortunate souls spending $50,000 a year in gas, then at least the Ink Bold will net yourself 2 roundtrip business class tickets to Europe just for using your Ink Bold!

Reason # 5: 5x at office supply stores

While this perk is not (quite) as effortless as moving your cellphone, internet, and cable bill over to your Ink Bold it can be still be beneficial for some people.

Many people with their own business need office supplies, and some people drop some major money on them.

Hello 5x!

Also, a lot of people forget that office supply stores like Staples and Office Depot also sell big ticket electronics, like computers and tablets. If you’re going to be buying an item like that (or even better, multiple ones), buy them there and rack up the points!

Reason #6: No foreign transaction fee and no annual fee for the first year

If you don’t already have a card with no foreign transaction fee, you should definitely add one to your wallet. Most credit cards will charge you 3% when you use it overseas, something that can add up very quickly.

Don’t let that vacation put you in the poorhouse!

Getting the Ink Bold solves this problem by charging you just the cost of your purchase, even when you are out of the country.

The Ink Bold also waives the annual fee for the first year, which is icing on the cake!

You’ll have a whole year to decide whether the perks of the card make it worth paying $95 for the second year, which for me is a resounding yes.

Final Word(s)

The Chase Ink Bold is undoubtedly a great card; not only does it have a pretty sweet signup bonus but it also has some killer perks that really allows you to rack up Chase UR points in a hurry with very minimal effort.

I would highly recommend it to anyone as long as they can make the $5,000 minimum spend in 3 months.

Click here to apply for the Chase Ink Bold

Want to profess your undying love for the Ink Bold as well? Have another card that is first in your heart? Haikus, soliliqoys and good old fashioned love letters accepted in the comments below!