If you decide to play the frequent flyer game with any regularity, there will inevitably come a time when you will be denied a credit card.

Even if you have a perfect credit score, low utilization rate, years of history with the card issuer and great standing, eventually you’ll end up with a denial letter or email.

You may be tempted to hang your head and rue a missed opportunity to earn even more miles.

If you’re only going to get one travel credit card, then the Chase Sapphire Preferred is an excellent choice.

It’s one of our favorite travel credit cards here at Extra Pack of Peanuts, and it was my go-to card for years (until Chase introduced the Sapphire Reserve).

Below, I’ll break down what makes the Chase Sapphire Preferred such an excellent card, but here are a few fast facts:

Earn 60,000 Chase Ultimate Rewards points after spending $4,000 in 3 months.

It’s not often that I am blown away by a credit card offer — but that changes with the Chase Sapphire Reserve.

Ever since Chase launched the Sapphire Reserve back in 2016, it’s been one of the best travel credit cards on the market.

I’ll break down exactly why below, but first, here are the important details:

Earn 50,000 Chase Ultimate Rewards points after spending $4,000 in 3 months.

$300 annual travel credit for spending on airfare, hotels, and other qualifying travel purchases.

3x on travel and dining and 1x on all other purchases.

Complimentary Priority Pass membership and a $100 credit for Global Entry or TSA PreCheck.

Sound too good to be true? Keep reading to find out all the ways this card can benefit you.

Why the Chase Sapphire Reserve Is the Best Credit Card for Travelers

The Chase Sapphire Reserve is one of our favorite travel credit cards.

So what exactly makes this card so great? Here are 7 things we love about the Chase Sapphire Reserve:

1. 50K Sign-Up Bonus with a Reasonable Minimum Spend

You’ll receive 50,000 Chase Ultimate Rewards points after spending $4,000 in the first 3 months.

Not only is 50k points a huge amount, but the minimum spend requirement of $4k in 3 months is pretty doable for most people.

2. Chase Ultimate Rewards Points

It gets better. Not only are you getting 50k points, but you’re earning the BEST travel points out there.

Chase points are my favorite because they can be used as cash through the Chase shopping portal, or they can be transferred to awesome partners like United, Southwest, and Hyatt (to name just a few).

At a minimum, these are worth $750 if you use them through the Chase portal. And if you transfer them, they can be worth $1500+.

Long story short: Chase points rule, and 50k is a lot of points.

3. $300 Annual Travel Credit

Each year, you’ll automatically get $300 in travel expenses reimbursed.

All you have to do is use your Chase Sapphire Reserve to purchase things that are coded as travel (flights, train tickets, etc.). This reimbursement is completely automatic and will show up as a statement credit.

4. Earn 3X Points on Travel and Dining

The Chase Sapphire Preferred used to be my go-to credit card because Chase points are highly valuable AND because it gives you 2x on travel and dining.

Now, the Chase Sapphire Reserve has upped the ante and gives you 3x on travel and dining.

This is awesome, especially for people who spend a decent amount on traveling and eating out.

5. Free TSA PreCheck or Global Entry

If all of that wasn’t enough, this card will reimburse you up to $100 when you sign up for TSA PreCheck or Global Entry.

TSA PreCheck will help you speed through domestic airport security, while Global Entry can save you lots of time when passing through border control both in the U.S. and abroad.

If you aren’t already a Global Entry member, we recommend getting that, as it includes TSA PreCheck.

6. Free Access to Priority Pass Lounges

All Chase Sapphire Reserve cardholders get free access to Priority Pass lounges. Priority Pass is a global network of airport lounges that offer perks such as free food, free alcohol, and free WiFi that actually works.

The lounges aren’t as luxurious as a nice hotel or restaurant, but they’re certainly nicer than the seats next to the gate.

7. No Foreign Transaction Fees

This is a standard feature with many credit cards, so Chase Sapphire Reserve isn’t special for offering it. Still, it’s a good benefit to have.

What Credit Score Do I Need for Chase Sapphire Reserve?

To qualify for the Chase Sapphire Reserve, you’ll need a Good/Excellent credit score. This generally means a score of at least 700, and ideally higher than 800. Given that the minimum credit limit for this card is $10,000, Chase wants to make you’re a responsible and experienced credit user.

Therefore, if you have average credit or just a limited credit history, we don’t recommend applying for this card. If your credit score is closer to 700, however, then it’s worth applying.

If you get rejected, you can always apply for the Chase Sapphire Preferred instead, which tends to be easier to qualify for.

Is the Chase Sapphire Reserve Worth It?

The answer depends on two factors:

How much you spend

How much you travel

Let’s take a closer look at each of these:

1. Can You Responsibly Spend $4,000 in 3 Months?

To start, if you wouldn’t ordinarily spend $4,000 in 3 months, then you shouldn’t get this card. You should never over-spend just to meet the minimum spend on a card; the math doesn’t make sense.

If $4,000 is too high, then we recommend looking into a card with a lower minimum spend, such as the Capital One Venture Rewards ($3,000 minimum) or Capital One VentureOne ($1,000 minimum).

2. Do You Travel Enough to Benefit from the Chase Sapphire Reserve Perks?

The Chase Sapphire Reserve is best for someone who travels frequently. At a minimum, you need to spend at least $300 per year on travel for this card to be worth it. Otherwise, it’s hard to justify the card’s $550 fee.

Furthermore, you need to regularly fly, stay in hotels, or do other travel-related activities to maximize the value of the Chase Ultimate Rewards points. If you tend to spend more on things like groceries and gas, then this isn’t the best credit card for you.

Our general rule is that if you travel more than 3x per year, get the Chase Sapphire Reserve. If you travel less than that, get the Chase Sapphire Preferred, which has a much lower annual fee.

Chase Sapphire Reserve vs. Preferred: 5 Key Differences

Before we conclude, there’s one more thing to address. Many people are curious about the differences between the Chase Sapphire Reserve and Preferred. The two cards share a lot of features and benefits, but there are also some key differences.

1. Chase Sapphire Preferred Has a Lower Annual Fee

The annual fee for the Chase Sapphire Preferred is $95, which is significantly less than the $550 annual fee for the Chase Sapphire Reserve. However, the $300 in annual travel credit that the Chase Sapphire Reserve offers effectively brings the fee down to just $250 if you travel regularly.

2. Chase Sapphire Preferred Has a Higher Sign-Up Bonus

Currently, you’ll earn 60,000 Chase Ultimate Rewards points when you spend $4,000 within the first 3 months of opening the Chase Sapphire Preferred. That’s 10,000 more points for the same minimum spend as the Chase Sapphire Reserve.

This difference is compelling, though you have to weigh it against the fact that the Chase Sapphire Reserve offers additional reimbursements worth up to $400 (see the next section).

3. Chase Sapphire Preferred Doesn’t Reimburse You for Travel Spending

While it’s tempting to think that the Chase Sapphire Preferred is the obvious choice given its lower annual fee and higher sign-up bonus, you also need to consider the value of the reimbursements that Chase Sapphire Reserve offers.

As we mentioned above, the Chase Sapphire Reserve will reimburse you up to $300 per calendar year for travel expenses such as airfare and hotel stays. They’ll also reimburse you up to $100 every four years for the Global Entry or TSA PreCheck application fee.

Given this, the Chase Sapphire Reserve has an effective annual fee of $250 per year (and only $150 for the first year if you apply for Global Entry). That’s still more than the Chase Sapphire Preferred, but the difference is less extreme than at first glance.

4. Chase Sapphire Preferred Earns Fewer Points for Travel and Dining

When you make travel or dining purchases with the Chase Sapphire Reserve, you’ll earn 3 Chase Ultimate Rewards points for every dollar you spend.

With the Chase Sapphire Preferred, however, you’ll only earn 2 points for every dollar you spend on travel and dining.

This isn’t a massive difference, and it really only matters if you spend a lot each month. Still, it’s worth noting.

5. Chase Sapphire Preferred Doesn’t Include Airport Lounge Access

The final important difference between the two cards is that the Chase Sapphire Preferred doesn’t include the airport lounge access that the Chase Sapphire Reserve gets you.

While this is a notable difference, it may not matter to you if you don’t spend a lot of time in airports. And while the lounges are nice, they’re far from luxurious.

Bottom Line

As soon as it was released, the Chase Sapphire Reserve became one of the best travel credit cards on the market:

The 50k sign up bonus is great, given that Chase points are the most valuable points out there.

The minimum spend is reasonable.

The $300 annual travel credit helps offset the annual fee.

Plus, you get 3x on travel and dining and a few other nice perks such as airport lounge access.

If you travel more than 3x per year and have a Good – Excellent credit score, I highly recommend you check this card out. Learn more about this card here.

[UPDATE: You can no longer use the steps below to pay your mortgage, student loans, etc. with a credit card. HOWEVER, there is another, even better way. Click here to learn how.]

Earning frequent flyer miles for big, recurring monthly bills, such as a mortgage, rent, or student loan payment, has been the holy grail of frequent flyers for years. They’ve searched high and low for ways to do it, but to no avail…

Until now!

Let me show you, step by step, just how to earn frequent flyer miles for paying your big monthly bills.

Step 1: Apply for a Bluebird card

How to do it:

Go to bluebird.com and sign up for your free Bluebird card.

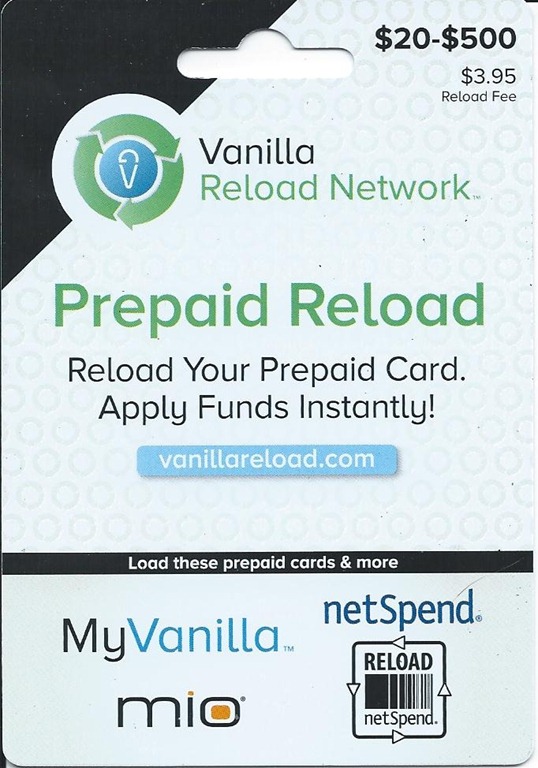

Step 2: Buy Vanilla Reload Cards At CVS with a Credit Card

CVs is the only place I know that allows you to buy Vanilla Reload cards with a credit card.

Make sure you are buying the Vanilla Reload card that looks EXACTLY like this:

Get the card that looks EXACTLY like this!

How to do it:

Find the Vanilla Reload cards that look exactly like the one above. Don’t buy anything that says Vanilla but doesn’t look the same (Frequent Miler has a great round up of all the Vanilla cards).

Make sure to load each Vanilla Reload card with $500. Again, you’ll have to pay the $4.95 activation fee regardless of the denomination, so always load with $500.

Pay for the Vanilla cards with your credit card.

Cost: $3.95 activation fee per card.

Step 3: Load the Vanilla Reload Cards on to Your Bluebird Card